By Lena Polnet, Mortgage Loan Originator | NMLS #17225

Published April 28, 2026

Pennsylvania state programs aren’t the only down payment assistance available. Montgomery County, Bucks County, and the City of Philadelphia each run their own first-time buyer assistance programs — and each one delivers up to $10,000 in forgivable money on top of, or instead of, PHFA programs. I’m Lena Polnet, mortgage loan originator at Dynamic Funding Solutions. If you’re buying in southeastern Pennsylvania, county-level programs are often the difference between renting another year and closing this summer.

Why County Programs Exist Alongside PHFA

The federal HOME Investment Partnerships Program sends money two ways: directly to states (PHFA in Pennsylvania), and directly to large counties and cities that meet HUD’s population and need thresholds. When a county or city receives its own direct HOME allocation, it runs its own program — and it’s typically excluded from PHFA’s HOMEstead pool to avoid double-dipping.

That’s why Philadelphia residents can’t use HOMEstead but can use Philly First Home. It’s why Montgomery County buyers have a county program in addition to K-FIT. Each county program is funded, capped, and administered locally — meaning rules, dollar amounts, and eligibility differ.

How county and PHFA programs interact

Most county programs can stack with PHFA first mortgages. A Montgomery County buyer can use Montgomery County’s $10,000 grant alongside a K-FIT loan, dramatically reducing cash to close. Confirm stacking rules with the specific county program before structuring the file — county allocations often include occupancy requirements that change the math.

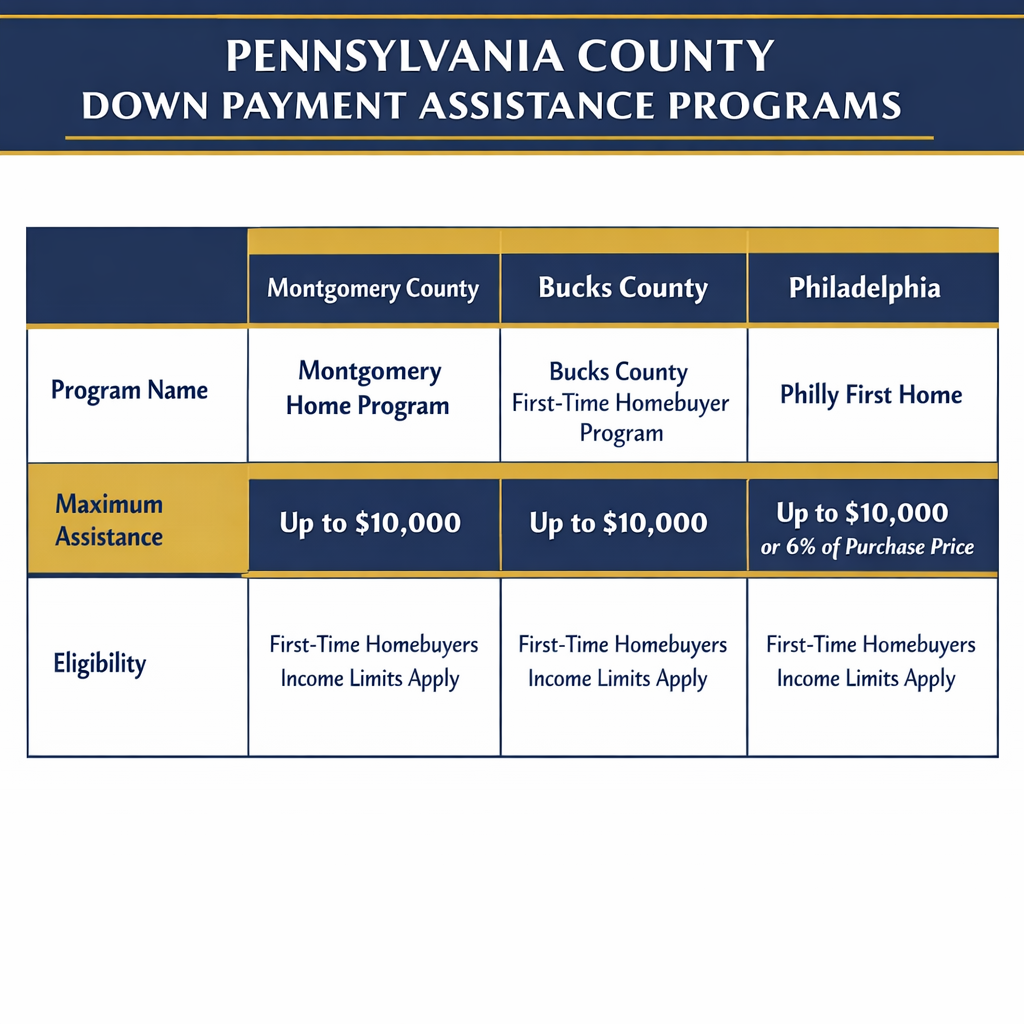

Montgomery County First Time Homebuyers Program

The Montgomery County First Time Homebuyers Program provides up to $10,000 — or 10% of the affordable sales price, whichever is lower — toward down payment and closing costs.

Montgomery County eligibility

- First-time buyer (no homeownership in past three years)

- Household income at or below Area Median Income for Montgomery County

- Currently reside OR work full-time in Montgomery County at application and closing

- Minimum $3,000 in liquid assets at application

- Must contribute 3% of sales price toward down payment from own funds (no gifts toward this 3%)

- Complete required homebuyer counseling before signing the agreement of sale

- Property must be primary residence in Montgomery County

Montgomery County terms

The grant is zero-interest and recaptures (becomes repayable) only if the home is sold, conveyed, transferred, vacated, or used as investment property within 15 years. Stay in the home 15 years and the assistance is fully forgiven. An additional $30,000 is available for households below 80% AMI through American Rescue Plan funding [Montgomery County website verified 2026-04-28].

Bucks County First Time Homebuyers Program

The Bucks County First Time Homebuyers Program provides up to $10,000 in down payment and closing cost assistance through a no-interest deferred mortgage.

Bucks County eligibility

- First-time buyer (no homeownership in past three years)

- Household income at or below 100% of Median Family Income for Bucks County, by family size

- One adult must have either six months residency in Bucks County OR one year continuous employment at a Bucks County workplace

- Property must be in Bucks County and used as primary residence

Bucks County terms

The Bucks County program structures assistance as a deferred mortgage — no interest, no monthly payment — that becomes due when the home is sold, transferred, refinanced for additional debt, or stops being the primary residence. There is no fixed forgiveness schedule; the lien sits silently until a triggering event.

Applications go through Bucks County Housing Group, which administers required counseling and walks applicants through intake.

Philly First Home

The Philly First Home program is the City of Philadelphia’s response to being excluded from PHFA’s HOMEstead pool. It provides up to $10,000 — or 6% of the home’s purchase price, whichever is lower — toward down payment, closing costs, or principal reduction.

Philly First Home eligibility

- First-time buyer (no homeownership in past three years)

- Income eligible per program tiers (varies by household size)

- Single-family home or duplex in Philadelphia (no condominiums)

- Complete one-on-one homeownership counseling through a City-funded agency before signing agreement of sale

Philly First Home terms

The grant is repayable only if the buyer moves out or refinances within 15 years. Stay 15 years and the grant is fully forgiven. Funding opens annually and is first-come, first-served — Philadelphia exhausts the pool every year.

How to Layer County Programs With PHFA

The strongest combinations for southeastern Pennsylvania buyers:

Montgomery County buyer: Montgomery County’s $10,000 + K-FIT (5% of purchase price) + an MCC. On a $400,000 Montgomery County home, that’s $10,000 + $20,000 = $30,000 toward closing, plus up to $2,000 annual federal tax credit.

Bucks County buyer: Bucks County’s $10,000 + K-FIT + MCC. Same math. Same stack.

Philadelphia buyer: Philly First Home $10,000 + a PHFA Keystone Government first mortgage + MCC. Philadelphia buyers cannot use HOMEstead (excluded county). They typically cannot stack K-FIT with Philly First Home depending on year-by-year program rules — confirm at pre-approval.

For a full comparison, see what nobody tells first-time home buyers in Pennsylvania.

What Most Buyers Get Wrong About County Programs

The first mistake is not knowing they exist. Most realtors don’t track county programs because the rules and dollar amounts change yearly. Buyers ask their lender about “first time buyer programs” and hear about FHA. They never hear about the $10,000 sitting at the county housing office.

The second mistake is treating county programs as a substitute for PHFA programs. They’re not. They’re additive. A Montgomery County buyer who uses ONLY Montgomery County’s $10,000 leaves K-FIT’s 5% and the MCC’s $2,000/year on the table.

The third mistake is missing the “currently reside or work in” requirements. Bucks County requires six months residency or one year of Bucks County employment. Montgomery County requires current residence or full-time employment. Buyers who quit a Bucks County job to take a job in New Jersey two months before closing lose program eligibility.

The fourth mistake is assuming counseling is optional or can happen after the agreement of sale. It can’t. All three programs require counseling completion BEFORE you sign a purchase contract. Sign first, lose the program.

Next Steps With Lena

County programs are the most situational of the assistance options — eligibility depends on which county the home is in, where you currently live or work, and which PHFA programs you’re already pursuing. The 15-minute call covers your specific county, your stacking options, and the counseling timeline so you don’t lose the program by signing a contract too early.

Frequently Asked Questions

Hover any row to expand. About = primary subject of this page. Mentions = referenced entity.

| Entity | Type | Role | Link |

|---|---|---|---|

| Montgomery County, Pennsylvania

First-time homebuyer program offers up to $10,000 forgivable after 15 years. Eligibility: reside OR work full-time in Montgomery County. Income and purchase price limits apply.

|

Pennsylvania County | About | Wikipedia |

| Bucks County, Pennsylvania

Deferred mortgage program (not forgivable) for down payment assistance. Repaid on sale, transfer, or refinance. Eligibility: 6 months residency or 1 year employment in Bucks County.

|

Pennsylvania County | About | Wikipedia |

| Philadelphia

Philly First Home program offers up to $10,000 (or 6% of purchase price) for first-time buyers. Must not have owned in past 3 years. Forgiven after 15 years of residency.

|

City / County | About | Wikipedia |

| Dynamic Funding Solutions

PHFA-approved mortgage lender operating in Montgomery, Bucks, Philadelphia and all PA counties. NMLS #17144. Lena Polnet NMLS #17225.

|

Mortgage Lender | About | Website |

| K-FIT (Keystone Forgivable in Ten Years)

PHFA statewide program stackable with county programs in some cases. Can combine K-FIT + Montgomery County for up to ~$30,000 in assistance on a $400,000 purchase.

|

Loan Program | Mentions | DFS Guide |

| Pennsylvania Housing Finance Agency

State agency. PHFA programs (K-FIT, HOMEstead, MCC) can often be layered with county programs for maximum assistance.

|

Government Agency | Mentions | Wikipedia |

- RelatedK-FIT — 5% Forgivable Down Payment Loan from PHFA

- RelatedHOMEstead Program — $10,000 Forgivable Down Payment

- RelatedMortgage Credit Certificate (MCC) for Pennsylvania Home Buyers

- RelatedWhat Nobody Tells First-Time Home Buyers in Pennsylvania

- CountyMontgomery County First Time Homebuyers Program

- CountyBucks County First-Time Homebuyer Program

- CountyPhiladelphia Philly First Home Program

- FederalHUD — Local Homebuying Programs by State

Talk to Dynamic Funding Solutions

County programs change yearly, stack differently with PHFA products, and require counseling completion before contract — meaning timing matters as much as eligibility. I’ll map your county, your residence/employment status, and your PHFA stacking options in 15 minutes.

Book a free 15-minute strategy call: calendly.com/lpolnet71/strategy_15min

Pennsylvania: (215) 364-7171

Florida: (561) 247-4888

Related reading: K-FIT: Keystone Forgivable in Ten Years | HOMEstead Program | Mortgage Credit Certificate (MCC) | How First-Time Home Buyer Programs Work

About the Author

Lena Polnet is a licensed Mortgage Loan Originator (NMLS #17225) with Dynamic Funding Solutions, serving home buyers across Pennsylvania and Florida. She specializes in stacking county-level down payment assistance with PHFA loan products for buyers in Montgomery, Bucks, Chester, Delaware, and Philadelphia counties. Lena coordinates directly with county housing offices and counseling agencies to keep buyer files compliant from intake through closing.

Legal Disclaimer

Dynamic Funding Solutions, NMLS #17144 | Lena Polnet, NMLS #17225 | Equal Housing Lender | Licensed in Pennsylvania and Florida.

This article is for informational purposes only and does not constitute a loan offer, commitment to lend, or financial advice. County program terms, dollar amounts, eligibility, and stacking rules change annually and vary by funding cycle — verify current rules with the administering county or city office before signing any agreement of sale. All loans are subject to credit approval, income verification, and property appraisal.